Ministry of Finance

Eastern Africa Statistical Training Centre

Chuo cha Takwimu Mashariki mwa Afrika

Latest News 📰

Upcoming Events 📅

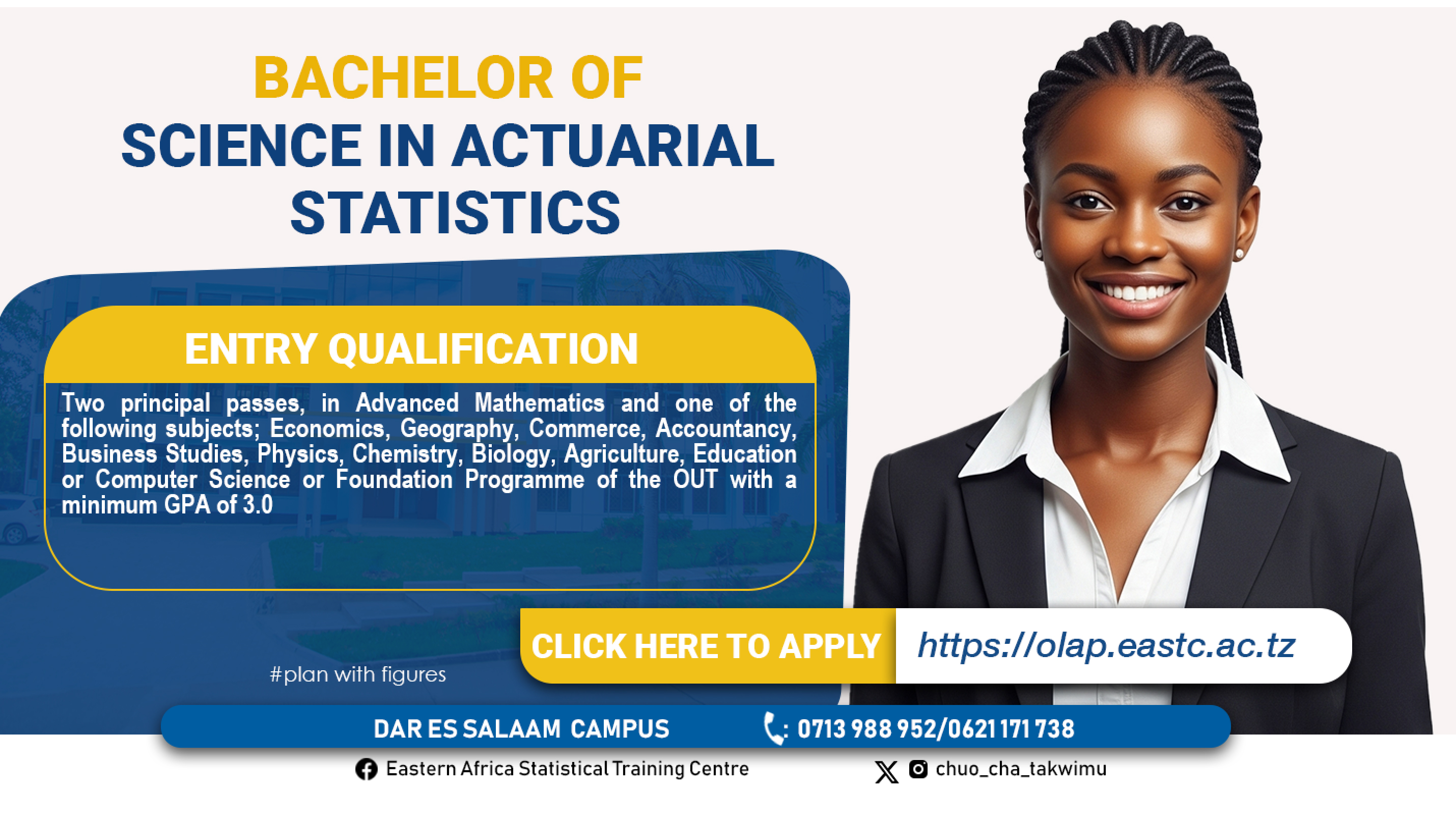

Release of Semester II/trimester III Provisional Examinations results

EASTC

August 5, 2025Marking and Processing of NTA 4-8 Second Semester Results begins

EASTC

July 15, 2025PRACTICAL TRAINING for NTA 5& 6 begins

EASTC

July 14, 2025

Dr. Tumaini M Katunzi

Welcome to the Eastern Africa Statistical Training Centre (EASTC), a regional centre of excellence committed to building the next generation of data-driven leaders and researchers.

Read more HEET PROJECT

HEET PROJECT

🌐 Visitor Counter

Vision

To be a centre of excellence in training Official Statistics in Africa.

Mission

To promote the production and use of high-quality statistics through training, research, and consultancy in statistics for evidence-based decision making in user countries.

Our Core Values

Integrity: Honest, truthful, and punctual.

Accountability: Answerable and complete duties on time.

Customer Focus: Providing services promptly.

Team Work: Full participation in achieving EASTC goals.

EASTC Stakeholders

We are proud to partner with an outstanding team of stakeholders.

Eastern Africa Statistical Training Centre

Plan with figures!

Quick Links

EASTC Collaborators

Related Links

- National Bureau of Statistics (NBS)

- World Bank

- Tanzania Commission For Universities (TCU)

- Higher Education Students' Loans Board (HELSB)

- The National Council for Technical and Vocational Education and Training (NACTVET)

- United Nations Economic Commission for Africa (UNECA)

- DataVision International

- East African Community (EAC)

- United Nations Statistical Commission

Contact

- Eastern Africa Statistical Training Centre

- P.O Box 35103

- Dar es Salaam, Tanzania

- Phone: +255 713 988 952

- Email: info@eastc.ac.tz

Copyright © All rights reserved | Eastern Africa Statistical Training Centre @pm